Bond-Market Investors Now Expect the US Fed to Start Slashing Its Policy Rate Soon

August 6, 2024How the Latest US Economic Data Have Impacted Fed Rate Cut Prospects

August 19, 2024

Last week Statistics Canada confirmed that our economy continued to shed jobs in July.

We lost 2,800 jobs on a net basis last month, following a net loss of 1,400 jobs in June. The latest result was well below the consensus forecast of +25,000.

Reactions to the July employment data were mixed, despite the discouraging headline number. That was true both in the bond market, where yields remained range bound, and among mainstream economists, who assessed that the positive and negatives in the latest employment data roughly balanced out.

The current consensus narrative goes something like this: The Bank of Canada (BoC) is concerned about weakening labour-market conditions, but that concern is tempered by the fact that wages are still rising by an average of 5% year-over-year.

The details in the latest employment data certainly justified the Bank’s increased focus on downside risks.

Our labour-force participation rate, which measures the percentage of Canadians who are either employed or seeking employment, is now the lowest it has been in more than 25 years. It fell from 65.3% in June to 65% in July.

While some economists are quick to point out that our aging population naturally puts downward pressure on our participation rate, we have also seen steady declines in the participation rates for both young workers (aged 15 to 24) and prime-aged workers (who range in age between 25 and 54).

Record immigration has increased the supply of labour much more rapidly than our economy’s demand for it, and that gap will widen further if businesses follow through on their plans to curtail hiring.

The latest employment data also confirmed that our public sector added 41,000 new positions last month while our private sector shed 42,000 jobs.

Our public sector is only one-third the size of our private sector, but despite that, it has added far more jobs than the private sector over the past twelve months (205,000 vs 86,000).

The current surge in public-sector hiring isn’t sustainable, it isn’t going to spur the productivity improvements that the BoC is desperately calling for, and bluntly put, it isn’t a healthy sign when public-sector hiring dwarfs private-sector hiring for an extended period.

Now let’s turn our attention to wage growth, which has been a burr in the BoC’s saddle for some time.

Average wage growth fell from 5.4% in June to 5.2% in July on a year-over-year basis.

That is still well above the level needed to return overall inflation to its 2% target, but probably not for much longer.

Average wage growth is set to fall sharply over the next two months and may well hit 2% by the end of this year thanks to base effects, which occur as monthly wage-growth prints roll out of Stats Can’s data set (because it only looks back over the most recent twelve months).

To see why, let’s take a closer look at the monthly wage-growth data:

- Average wage growth increased by 0.7% last August, and by 1.61% last September on a month-over-month basis. These two monthly prints will roll out of Stats Can’s data set over the next two months and be replaced by the wage-growth results for August and September this year.

- Wages have increased by an average of 0.22% (month-over-month) thus far in 2024, and over the most recent three months, that average growth rate has slowed to 0.19%. (To err on the conservative side, we’ll use the year-to-date average.)

- If our average month-over-month wage growth comes in at 0.22% in August and September, our year-over-year average wage-growth rate will fall from 5.2% in July to 4.6% in August and will then drop all the way down to 3.2% in September.

- If we project average monthly wage growth of 0.22% for the remainder of the year, which is not a stretch considering our deteriorating employment backdrop, our average year-over-year wage growth will be down to 1.95% by the time we’re all singing Auld Lang Syne.

Today, bond-market investors are betting on BoC rate cuts of 0.25% at each of its three remaining meetings in 2024. I don’t think such a sharp drop in wage growth is yet built into most forecasts.

If wage growth follows that path, bond yields, and the fixed mortgage rates that are priced on them, should move lower, and we may also see at least one BoC rate cut of 0.50% being priced in.

Imagine most of that happening before the leaves are even off the trees. The Bottom Line: Government of Canada bond yields held mostly steady last week, stabilizing after their big drop the week prior.

The Bottom Line: Government of Canada bond yields held mostly steady last week, stabilizing after their big drop the week prior.

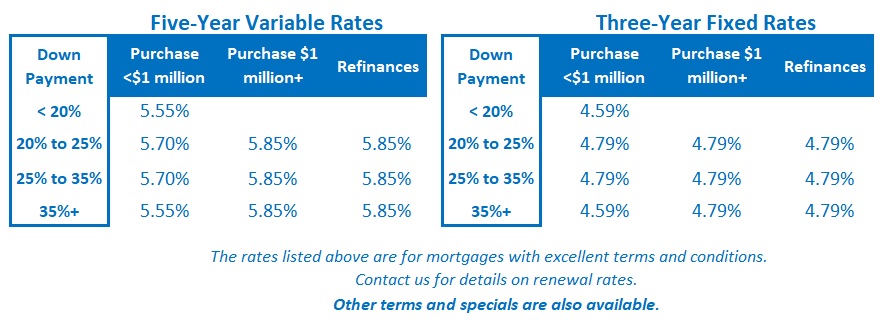

Lenders continued to drop their fixed mortgage rates in response, and the laggards will continue to catch up this week.

Variable-rate discounts were unchanged.

The bond futures market is currently pricing total BoC rate cuts of 0.75% by the end of this year. If average wage growth falls as much and as fast as I expect, that will increase the Bank’s flexibility to lower even more.

The backdrop for variable-rate mortgages continues to improve.