A Warning About Canadian Fixed Mortgage Rates

November 18, 2024What Disappointing GDP Growth Means for Canadian Mortgage Rates

December 2, 2024 Last week Statistics Canada confirmed that our Consumer Price Index (CPI) increased to 2.0% in October, above the consensus forecast of 1.9%.

Last week Statistics Canada confirmed that our Consumer Price Index (CPI) increased to 2.0% in October, above the consensus forecast of 1.9%.

The Bank of Canada’s (BoC) most closely watched measures of core inflation, CPI-median and CPI-trim, also increased from an average of 2.4% in September to 2.6% in October.

Bond-market investors responded to the higher-than-expected inflation data by reducing the odds of a 0.50% rate cut by the BoC at its next policy-rate meeting on Dec 11.

I think that was an over-reaction.

While there are still pockets of inflation that concern the Bank, rising food prices chief among them, our longer-term inflation trends are still mostly encouraging:

- Inflation in mortgage interest costs, which remains the primary source of our current inflation pressure, decelerated last month. Those costs still increased by 14.7% year-over-year (YoY) in October, but that was down from +16.7% in September. Further deceleration is baked in now that mortgage rates have declined markedly from their peaks.

- Rental cost increases, another key inflation driver, also cooled last month, decelerating from 8.2% YoY in September to 7.3% in October. A further cooling in rental costs is expected as immigration falls.

- When shelter costs are excluded, our CPI increased by only 0.9% YoY in October.

- Inflation in service prices decreased from 4% YoY in October to 3.6% in September.

- Goods inflation increased a little last month, but only by 0.1% YoY. That should be of little concern to the Bank in the face of weaker spending data and bloated inventory levels.

Last month’s slight uptick aside, inflation is still bang on the BoC’s 2% target and, equally importantly, the inflation expectations of consumers and businesses have now normalized.

With inflation pressures no longer forcing the Bank’s hand, it can shift the focus of its monetary policy to our softening labour-market and weak GDP data. (Our GDP has declined on a per-capita basis for five consecutive quarters.)

The Bank’s policy rate currently stands at 3.75%, a restrictive level that is reducing demand at a time when our inflation data no longer call for that treatment. The policy rate will continue to be a headwind for our economy until it is reduced to a range between 2.5% and 3.0%. It is now practically a forgone conclusion that the Bank will cut to at least that range.

Inflation has fallen much faster than the Bank anticipated, even though its policy-rate changes take at least a year before their impacts are fully realized. That delay increases the probability that the Bank has already overtightened by leaving its policy rate this high for this long, and it now needs to hustle to course correct.

In that context, one slightly higher-than-expected inflation report shouldn’t change much.

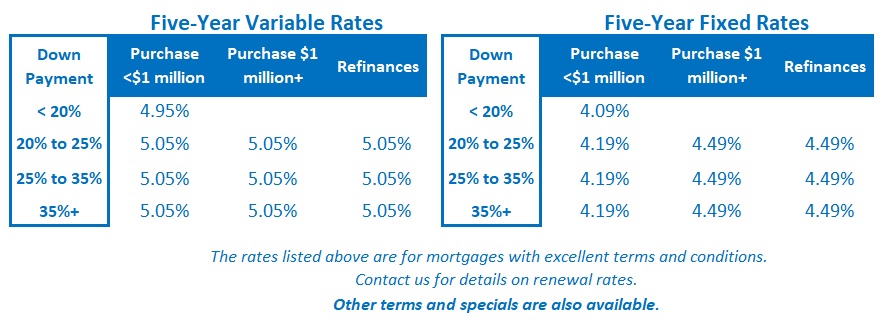

Mortgage Advice for Now

If you are a conservative borrower who prefers the stability of a fixed payment, I think today’s fixed mortgage rates have likely bottomed for the time being.

They are based on Government of Canada (GoC) bond yields. These already have a lot of good news priced in, such as our CPI’s return to its 2% target and the nearly universal expectation of at least another 1% drop in the BoC’s rate over the near term.

If fixed mortgage rates are going to fall further, it will have to be because of a new and currently unforeseen catalyst.

For now, the newly emerging catalyst that is currently impacting GoC bond yields is the election of former US President Trump to a second term.

Bond market investors have responded by pushing US Treasury yields steadily higher as they price in higher US inflation ahead, and GoC bond yields have been taken along for the ride. That upward pressure on bond yields, and therefore our fixed mortgage rates, shows no signs of abating at this point.

The near term looks very different for our variable mortgage rates.

Additional BoC rate cuts of at least 1% appear all but inevitable at this point, and our variable mortgage rates will decrease in lockstep. I also think there is a good chance that the Bank will be compelled to cut further as it becomes clearer that it left its policy rate too high for too long.

Nonetheless, the lowest-priced variable rates come with five-year terms, and anyone choosing a variable-rate today should be fully prepared for their rate to move in both directions over that time horizon.

On balance, based on my assessment of where we are in our current interest-rate cycle, I think our variable mortgage rates are likely to save money over today’s fixed-rate options. The Bottom Line: For the reasons outlined above, I expect our fixed and variable mortgage rates to move in opposite directions over the near term.

The Bottom Line: For the reasons outlined above, I expect our fixed and variable mortgage rates to move in opposite directions over the near term.

Government of Canada (GoC) bond yields rose last week in response to our higher-than-expected inflation data and the strong gravitational pull of steadily rising US Treasury yields.

Some lenders have started to increase their fixed mortgage rates in response, and I expect others to follow this week.

I will wait for the next rounds of our employment and GDP data before making a call on whether the BoC will cut by 0.25% or 0.50% at its next meeting on December 11. But in the meantime, I don’t think last week’s inflation data will cause the Bank to alter its plans.

This simple fact remains: The Bank’s policy rate is too high and variable-rate borrowers can reasonably expect several more cuts ahead.