Last Week’s Surprising Bond-Market Moves Are Good News for Canadian Mortgage Rates

December 9, 2024Happy Holidays

December 23, 2024

.

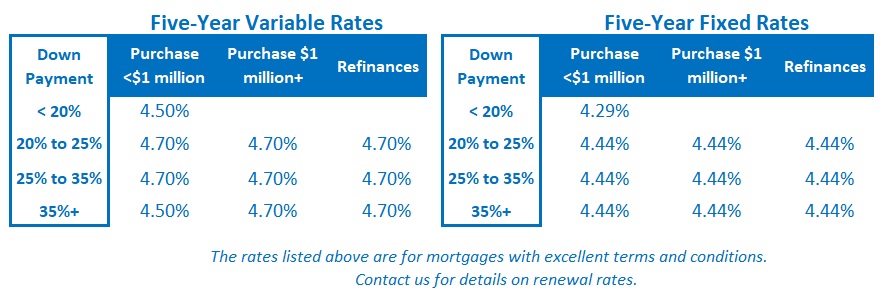

Last Wednesday, the Bank of Canada (BoC) cut its policy rate by another 0.50%, as expected. That means our variable mortgage rates will be reduced by the same amount in short order.

Our fixed mortgage rates were unchanged last week, in part because the Government of Canada (GoC) bond yields, which they are priced on, had already dropped in anticipation of the BoC’s latest cut.

Here are my five key takeaways from the Bank’s most recent policy statement and accompanying press conference.

- The BoC is done with 0.50% cuts, but further policy-rate reductions should still be in store.

BoC Governor Macklem said the Bank will adopt “a more gradual approach” to additional policy-rate changes from here. That means we should expect further cuts to be in 0.25% increments (but it doesn’t mean that that its policy rate won’t be reduced further).

The Bank’s policy rate currently stands at 3.25%, which is at the upper end of what the BoC considers its neutral-rate range (which is defined as the level where its policy rate is neither restricting nor stimulating demand).

But the Bank considers a neutral policy rate to be appropriate when “the output gap is closed, inflation is at target and there are no shocks pushing the economy around.” (Clarification: The output gap measures the gap between our economy’s actual output and its maximum potential output.) Those conditions are not consistent with our current backdrop.

Right now, we have an output gap that is widening; there are material shocks “pushing our economy around”; and we have the looming threat of much more severe shocks ahead.

A policy rate at the upper end of its neutral range simply doesn’t provide enough of a buffer to insure against those downside risks.

Clearly, more cuts are still needed. How many will we see?

If past is prologue, quite a few.

Economist David Rosenberg recently noted that the BoC’s policy rate bottomed out at “no higher than 2%” over its last five rate-cut cycles.

- The BoC has consistently over-estimated our economy’s growth trajectory.

The Bank has been basing its monetary-policy decisions on assumptions that are proving too optimistic. Those over-estimates imply that it has left its monetary policy too tight for too long and that deeper cuts will now be needed to course correct.

Governor Macklem has acknowledged that our Q3 GDP growth of 1% was “slower than we expected”, that recent data indicate that “growth will be lower than projected in the final quarter of this year”, and that “reduced immigration targets … suggest GDP growth next year will be lower than we forecast in October”.

Despite those candid assessments, the BoC may not be finished erring on the high side.

At his press conference Q & A, Governor Macklem said that he doesn’t think Canada is headed for a recession. From that, we can infer that he doesn’t think that we are already in one, despite our GDP-per-capita having fallen for eight of our last nine quarters.

- Canada’s primary economic growth engines haven’t changed.

The BoC’s forecasts have long been based on the prediction that more of our economic growth would come from export sales and business investment, with less coming from consumer spending and housing investment.

When the Bank sharply increased its policy rate, consumer spending and housing investment lagged because they are highly sensitive to interest-rate changes. But increased export sales and business investment did not materialize, and we were left with an economy rolling along at just a little over stall speed.

Even now that rates have fallen, the Bank notes encouraging pick-ups in consumer spending and housing activity, but also notes that overall economic growth is being “pulled down” by business investment and exports.

Plus ça change ….

- The weaker Loonie isn’t causing the BoC to alter its plans.

Last week, in an interview with Mark Rendel of the Globe and Mail, Governor Macklem was asked to comment on the divergence between the BoC and Fed policy rates and its impact on the Loonie, which has weakened steadily against the Greenback.

Macklem responded that there have been other periods with “large divergences”, that we’re “a little over one percentage point” right now, and that “it’s certainly been wider than that in the past”. (For reference, the widest divergence was 2.5% in 1997.)

He explained that the impact of the policy-rate divergence on the Loonie was an “open question” because Canada’s exchange rate versus other countries “has not changed very much”. Instead, he assessed that the Loonie’s recent depreciation against the Greenback “is more reflective of US dollar strength” against all other currencies.

At this point, it doesn’t appear that the weaker Loonie is significantly impacting the BoC’s policy-rate plans.

- The BoC acknowledged the negative economic impact of tariff threats.

The Bank noted “the possibility of new tariffs on Canadian exports to the United States” as a “major new uncertainty”.

Government Macklem acknowledged that even the threat of tariffs will likely hurt business confidence and impact business investment plans.

While he said the Bank won’t respond pre-emptively, it is reasonable to infer that, at the very least, the Bank will be counting trade uncertainty as a new headwind for our economy going forward.

Mortgage Advice for Now

I expect more BoC rate cuts ahead, and I continue to believe that variable mortgage rates will produce the lowest cost for borrowers over their typical five-year terms.

That said, the recent elevated economic and geopolitical instabilities are a reminder that circumstances can change quickly. Anyone choosing a variable-rate today should only do so if they are prepared for that rate to move in both directions.

I think more conservative borrowers who prefer the stability of a fixed rate no longer need to shy away from longer fixed-rate terms.

For example, five-year fixed rates are now below their long-term averages, and the GoC bond yields they are priced on are being pulled along by their rising US Treasury equivalents.

Simply put, if US Treasury yields rise, it is almost certain that Canadian fixed mortgage rates will follow. The Bottom Line: GoC bond yields moved higher last week due to several factors:

The Bottom Line: GoC bond yields moved higher last week due to several factors:

- Investors often “buy the rumour” in the lead up to an event (like expected rate cuts), and then “sell the fact” when the actual event occurs.

- The BoC’s guidance that it will take a more “gradual approach” reduced the bond market’s expectations for further cuts.

- The latest US inflation data caused US bond-market investors to price in fewer Fed rate cuts ahead. US Treasury yields moved higher as part of that response, taking GoC bond yields along for the ride.

GoC bond yields have been all over the map lately, but at their current levels, they probably aren’t putting too much pressure on our fixed mortgage rates in either direction.

Variable-rate discounts were unchanged last week.

I expect the BoC to continue reducing its policy rate in early 2025. If I’m right, that means our variable mortgage rates still have room to fall further from here.