The US Federal Reserve Is as Uncertain as Everybody Else

March 24, 2025How Trump’s Tariff Tirade Is Impacting Canadian Mortgage Rates

April 7, 2025 Last week Statistics Canada released our latest GDP data. The results were better than expected, for the second month in a row, mostly because buyers were front running US President Trump’s tariffs.

Last week Statistics Canada released our latest GDP data. The results were better than expected, for the second month in a row, mostly because buyers were front running US President Trump’s tariffs.

Normally I could analyze the data and draw implications for the near-term direction of Canadian mortgage rates. But, at the moment, those data aren’t much help.

Our near-term economic outlook is in flux thanks to ever-changing tariff threats.

The next round of tariffs, which President Trump has referred to as “the big one”, are supposed to be announced this Wednesday. If past is prologue, the initial levies will be dramatic, the US stock market will immediately sell off, and Trump will respond by reducing most of them (while declaring victory with each reduction).

Simply put, President Trump loves chaos, and he’s got 1390 days left in office.

Instead of hoping that things will settle down at some point, I think we are better served by assuming that we will remain in this volatile economic environment for as long as he is calling the shots.

With that in mind, here is my detailed take on the pros and cons of fixed and variable mortgage rates in this trade-war era.

The Case for a Variable-Rate Mortgage

I expect the Bank of Canada (BoC) to continue cutting its policy rate, which our variable mortgage rates are priced on, for the following reasons:

- The negative economic impacts from US tariffs are the BoC’s most pressing concern.

- The BoC’s policy rate is currently 2.75%, which it estimates to be in the middle of its neutral range (the level where its policy rate is neither constraining nor stimulating demand). The Bank’s policy rate won’t be considered stimulative until it hits 2%. I think the Bank will continue cutting at least until it reaches that level.

- A policy rate of 2% would also be consistent with the BoC’s past playbook. The Bank has reduced its policy rate to 2%, or lower, during each of its five most recent rate-cut cycles.

- Our most recent inflation data came in hotter than expected, but the BoC’s monetary-policy tools are far better suited to fighting inflation than fighting deflation (which may occur if our economy falls into recession). For that reason, I think the Bank would rather deal with a little too much inflation, rather than not enough of it.

- If our government responds to Trump’s tariffs with counter-tariffs, that will be inflationary. But the BoC has said that it will look through any one-time, tariff-related price hikes. If inflation pressures broaden because companies unaffected by tariffs enact opportunistic price increases, as happened during COVID, that will concern the BoC. But that seems unlikely because consumers will be less able (and willing) to absorb price increases this time around.

- Near-term consumer and business inflation expectations have increased of late. That will concern the BoC. But BoC Governor Macklem recently noted that the Bank is paying closest attention to medium and long-term inflation expectations, and they remain within historically normal ranges.

- This year, approximately one million Canadian mortgage borrowers will renew the ultra-low mortgage rates they locked in during the pandemic. Rates are higher now, so these borrowers will all face a payment shock. Additional BoC rate cuts will help to lessen it.

While the BoC may decide to pause at its next meeting on April 16, I still expect more near-term cuts to be forthcoming. Over the longer term, I think that the powerful negative impacts from Trump’s tariff policies will act as a brake on the economy, which will dampen demand and keep downward pressure on rates.

There is certainly a risk that the BoC will need to raise its policy rate at some point over the next five years (which is the most common variable-rate mortgage term), but I don’t think that substantial increases will be required.

Variable-Rate Pros

- Variable rates will adjust immediately if the BoC enacts more rate cuts (and I expect that it will).

- Variable rates are likely to stay low during a sustained period of economic weakness (which I foresee).

- Optionality can be important. Variable rates are convertible to fixed rates at any time, and at no cost. (Borrowers must convert to a fixed-rate term that is equal to or greater than their remaining variable-rate term.)

- If you need to break your mortgage before the end of its term, variable-rate penalties are almost always capped at three months’ interest (which is the lowest penalty charged on any closed mortgage).

- Some variable-rate mortgages come with fixed payments that do not automatically adjust when their rate changes (unless the rate increases to the point where that fixed payment is no longer covering the interest cost). Borrowers who choose fixed-payment variable rates typically also have the option to voluntarily adjust their payment if desired.

Variable-Rate Cons

- Variable rates have the potential to increase by much more than can be expected in advance, and nobody rings a bell when it’s time to lock in.

- Today’s variable rates are higher than their fixed-rate equivalents (so anyone choosing this option today is doing so on the bet that rates will continue to fall from here, perhaps for the reasons I outlined above). The higher starting rate also makes today’s variable mortgages a little harder to qualify for.

- The fixed rates offered by lenders at conversion are typically not as competitively priced as those offered to new customers.

- Variable rate discounts are often reset, and can be reduced, when variable-rate mortgages are ported to a different property.

The Case for a Fixed-Rate Mortgage

Most of the borrowers I work with today are opting for the stability of a fixed rate. They already have enough uncertainty in their lives without worrying about where their mortgage rate is headed.

You can’t put a price on a good night’s sleep, and for that reason, a fixed rate is never really a bad option, even if it ends up costing more.

Mortgage payments are typically a significant household expense, and a fixed rate provides a form of cash-flow insurance. This can be especially important for first-time buyers, who are assuming home-ownership costs for the first time.

Just as with other forms of insurance, even if you didn’t need it in hindsight because rates didn’t end up rising, the cost of the protection is still easy to justify. For example, people don’t regret paying for fire insurance because their house didn’t burn down.

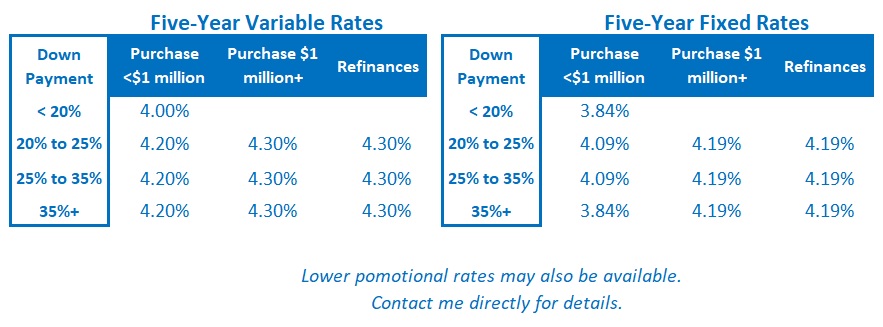

Today’s fixed rates have fallen significantly from their recent peaks and are now below their long-term averages. Bond-market investors have also begun to price in tariff-related economic weakness to the Government of Canada (GoC) bond yields that our fixed rates are based on.

For borrowers who prefer the certainty of a fixed rate, I think terms of between three to five years are the best options. Today all those terms are available at similar rates. Shorter one- and two-year fixed-rate terms are only available at much higher rates, which I still don’t think are worth paying.

Fixed-Rate Pros

- Fixed rates offer stability and peace-of-mind.

- Today’s fixed rates are well below their recent peaks and have already dropped in anticipation of economic weakness ahead.

- Today’s fixed rates are typically a little lower than today’s starting variable rates. That means they will save borrowers some money at the outset and they are also a little easier to qualify for.

- Fixed rates are never reset when the mortgage is ported over to a different property.

- A fixed-rate term of three years or longer will provide rate certainty over most, or all, of President Trump’s current term.

Fixed-Rate Cons

- Fixed rates eliminate the potential for additional interest-rate saving until the end of the locked-in term.

- If you need to break your mortgage before the end of its term, fixed rates come with penalties that are usually much higher than those charged for variable rates. (Importantly, there are also significant differences in the way fixed-rate interest-differential penalties are calculated, which you can learn more about here.)

- Fixed rates aren’t convertible to variable rates.

The Bottom Line: GoC bond yields dropped a little last week. Their next big move will likely be in response to the US tariffs that are set to be announced this Wednesday.

Fixed mortgage rates were unchanged last week. I expect them to drop if bond yields continue to trend lower, although not by as much as we would typically expect because credit spreads have also continued to widen.

Widening credit spreads have also led to a reduction in the variable-rate discounts offered by lenders.

The bond market now assigns about a 40% probability that the BoC will cut at its next meeting on April 16. Regardless, I continue to think that more BoC rate cuts are in store, and if I’m right, variable rates have farther to fall.