Why Canada’s Strong GDP Growth Hasn’t Impacted Our Mortgage Rates

March 3, 2025Thoughts on the Bank of Canada’s Latest Rate Cut

March 17, 2025 Last week, Statistics Canada confirmed that our employment growth slowed in February.

Last week, Statistics Canada confirmed that our employment growth slowed in February.

Our economy generated only 1,100 new jobs. That result was way below the consensus forecast of 20,000 and stood in sharp contrast to the robust growth seen in the three prior months.

The detailed data were also mostly disappointing.

Full-time positions declined by 19,700 while part-time positions increased by 20,800, average hours worked declined by 1.3% (mostly attributed to bad weather), and our population growth (+47,000) dwarfed new job creation.

Furthermore, as per CIBC economist Andrew Grantham, “the sector composition for employment suggests some weakness in areas most at risk from tariffs (transportation and warehousing and manufacturing).”

The tailwind from lower rates, which had been giving our economy a boost, is now being counteracted by a headwind created by US President Trump’s trade-war threats.

As per economist David Rosenberg, this period of “super-elevated uncertainty” will “shelve capex plans [aka business investment], cause a rise in the personal savings rate, and lead to risk-averse behaviour in financial markets”, which will include “wider credit spreads”.

When credit spreads widen, lender funding costs increase. That weakens the correlation between fixed mortgage rates and Government of Canada (GoC) bond yields.

Bond-market investors now assign an 80% probability that the Bank of Canada (BoC) will enact another 0.25% cut when it meets this Wednesday. As per my previous post, I expect that to happen for the following reasons:

- US trade-war threats are now the BoC’s primary concern.

- The BoC’s monetary-policy tools are far better suited to fighting inflation than deflation (which has now become a looming risk). For that reason, all else being equal, the Bank would rather err on the side of engendering too much inflation rather than too little.

- The BoC’s policy rate is currently 3%, which it estimates to be the upper end of its neutral range (the level where its policy rate is neither constraining nor stimulating demand). The Bank’s policy rate won’t be considered stimulative until it hits 2%. I think the Bank will continue cutting until it gets closer to that level.

- A policy rate of 2% would also be consistent with the BoC’s past playbook. The Bank has reduced its policy rate to 2%, or lower, in each of its five most recent rate-cut cycles.

- This year, a substantial number of Canadian mortgage borrowers will have to renew the ultra-low mortgage rates they locked in during the pandemic. Rates are higher now, so they all face a payment shock. Additional BoC rate cuts will help lessen it.

- Consumer and business inflation expectations have now returned to their historically normal ranges, thereby increasing the BoC’s flexibility to become more accommodative.

I had expected the BoC to cut this week even before we learned that our employment momentum slowed in February. The recent data bolster that expectation.

Put me down for a 0.25% cut this Wednesday (with an outside chance the BoC cuts by 0.50% instead). The Bottom Line: Government of Canada (GoC) bond yields finished the week about where they started it.

The Bottom Line: Government of Canada (GoC) bond yields finished the week about where they started it.

Despite that, some major banks reduced their lowest advertised fixed rates as it became increasingly apparent that bond yields have reset into a lower trading range.

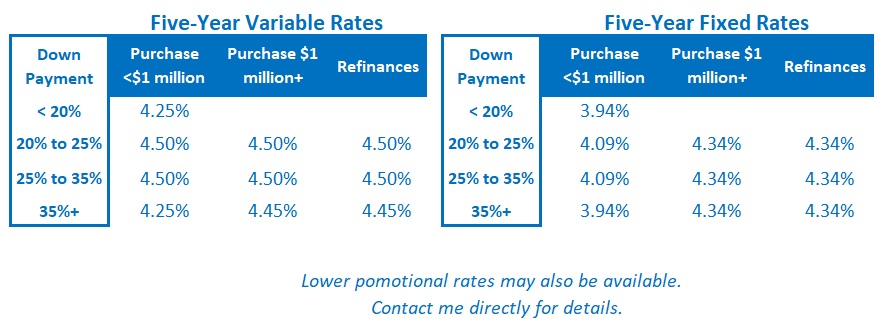

As a reminder, fixed mortgage rates don’t respond directly to the BoC’s policy-rate changes. They are priced on GoC bond yields, which incorporate the Bank’s expected policy-rate path, along with other many other factors, such as the direction of US Treasury yields.

Bond-market investors have already priced a BoC rate cut of 0.25% this week. As such, GoC bond yields may not move much if the Bank’s accompanying commentary is in line with expectations. That said, trade-war uncertainty will likely keep downward pressure on bond yields, and our fixed mortgage rates, moving forward.

Variable-rate mortgage borrowers are likely to see their rates drop by another 0.25% this Wednesday. And if my read of the tea leaves is prescient, there will be more BoC rate cuts still to come.

2 Comments

Just want to say Thank you Dave. I appreciate reading your blog weekly.

Perry

Thanks Perry. Nice of you to say. 🙂