A Mortgage Stress-Test Change at Last

September 30, 2024Monday Morning Interest Rate Update

October 15, 2024 Last week provided a reminder of why bond yields and mortgage rates are so difficult to forecast.

Last week provided a reminder of why bond yields and mortgage rates are so difficult to forecast.

Government of Canada (GoC) bond yields had been on a steady downtrend in July, August and September as our inflation continued to cool and our economic data continued to weaken.

In late September, Statistics Canada confirmed that our Consumer Price Index (CPI) returned to its 2% target in August. Shortly thereafter the US Federal Reserve announced a 0.50% cut to its policy rate and indicated that more cuts would follow. The wind was at our backs.

But then, just when it seemed inevitable that mortgage rates would continue to melt lower, bond-yield momentum turned.

Oil prices rose steadily last week as geopolitical tensions in the Middle East increased from a simmer to a boil. The cost of a barrel of WTI crude oil surged a full 10% higher.

That is concerning for inflation, because oil prices and overall inflation tend to move in the same direction. Oil prices have a pervasive impact on other costs throughout an economy – both directly, as a significant energy cost, and indirectly, as an input cost to produce plastics.

The Bank of Canada (BoC) cited geopolitical risks as one of its two main upside risks to its inflation outlook in its most recent Monetary Policy Report (on page 28). The Bank’s concerns include the risk that wars “could impact global commodity prices and impede the supply of traded goods”.

On Friday, steadily rising oil prices met with a banner US employment report.

The latest US non-farm payroll numbers confirmed the US economy added an estimated 245,000 new jobs in September, well above the consensus forecast of 150,000. The initial estimates for July and August were also revised higher by 72,000.

Last week’s combination of a war-linked surge in oil prices and stronger-then-expected US job creation led to the biggest swing in bond yields that we have seen in a while.

The benchmark 10-yr US Treasury yield increased by 0.22% last week. and that move took GoC bond yields along for the ride.

It hasn’t been long since the Fed’s 0.50% rate cut– the one that was deemed necessary to bolster employment momentum and permissible because inflation was cooling.

Fast forward another seven days, and oil prices are changing the inflation narrative and the US employment market doesn’t look as though it needs the Fed’s help.

We’re on a bumpy path.

Mortgage Selection Advice for Today (with some words of caution)

I still think more BoC cuts are on the way, although last week is a reminder that events don’t always play out as expected (or hoped) and that the timing and magnitude of future cuts are still uncertain.

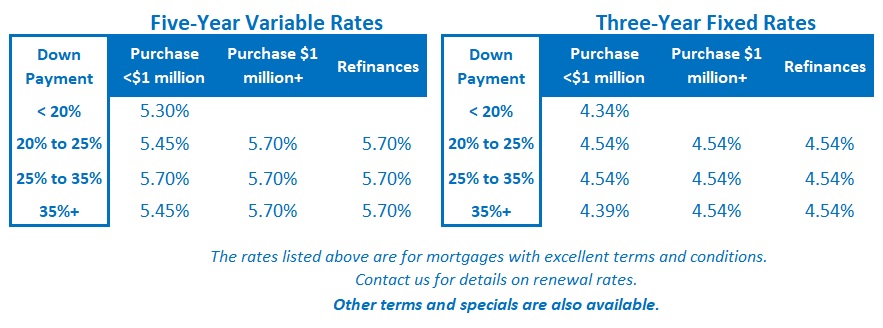

If you think they’re headed lower over time (and I do), variable rates should compare favourably to today’s fixed-rate options.

The consensus forecast right now is that the BoC will steadily reduce its policy rate from its current level of 4.25% to a level between 2.5% and 3% by the end of 2025. That would reduce today’s variable rates by at least 1.25% from their current levels.

More conservative borrowers, who prefer the stability of a fixed rate mortgage, will likely see those rates increase soon.

Bond-market investors had priced a series of near-term cuts by the BoC into the GoC bond yields, which our fixed mortgage rates are priced on. That pushed them lower.

Fast forward to now.

If the bond-market’s expectations around the timing and magnitude of those BoC cuts are dialed back, GoC bond yields, and our fixed mortgage rates, will move higher. Especially if oil prices keep rising and the US economy continues to chug along.

It suddenly appears that our fixed rates have bottomed, for now, and will likely move higher, at least over the near term. The Bottom Line: Bond yields surged higher last week for the reasons outlined above.

The Bottom Line: Bond yields surged higher last week for the reasons outlined above.

Our benchmark (for mortgage rates) five-year GoC bond yield surged higher by 0.29%. Lenders have initially responded by pulling back some of their most aggressively priced promotional fixed rates.

If the upward momentum in bond yields carries over into this week, a round of increases to our fixed mortgage rate will not be far off.

Variable-rate borrowers should still expect additional BoC rate cuts ahead, but maybe not at the same pace. For example, last week’s developments reduced the likelihood that the Bank will cut by 0.50% at its next meeting on October 23.