Canadian Mortgage and Real-Estate Predictions for 2025

January 6, 2025Implications for Last Week’s Mortgage-Rate Related News

January 20, 2025

Last Friday we received the latest US and Canadian employment reports, for December, and both headline prints came in higher than expected.

Bond yields on both sides of the 49th parallel spiked in response, adding upward pressure to Government of Canada bond yields, which our fixed mortgage rates are priced on.

A closer look at the data confirms that the strong response from bond-market investors was more appropriate for the US results than for the Canadian results.

The US economy added an estimated 256,000 new jobs last month, well above the consensus forecast of 165,000. Almost all the new jobs (223,000) were created in the private sector; the unemployment rate fell from 4.2% in November to 4.1% in December; and average hourly wage growth clocked in at 3.9%, which is well above the current US inflation rate of 2.7%.

That was all good news for US economic growth, but bad news for anyone hoping for more rate cuts from the US Federal Reserve. US inflation has now increased for three consecutive months, and we will probably learn this Wednesday that it moved higher again in December.

Accelerating inflation, a hot labour market, and the increased purchasing power for US consumers (who account for about 70% of total US GDP) have compelled bond-market investors to recalibrate their forecasts of the Fed’s policy-rate path in 2025.

Investors are now pricing in only one 0.25% cut by the Fed this year, and the benchmark 10-year US Treasury yield, which had already been on a tear, spiked higher by another 0.10% immediately following the release of the latest US employment data.

If the Fed’s reaction to the latest US employment data was a concern, the BoC’s reaction to the latest Canadian employment data was more likely relief.

The Canadian economy added an estimated 91,000 new jobs last month, also much higher than the consensus forecast of 25,000. Our unemployment rate decreased from 6.8% in November to 6.7% in December; our average hours worked increased by a robust 0.5% last month; and our average wages increased by 3.7% year-over-year (well above our current inflation rate of 1.9%).

While the Canadian employment data showed improvements that were like the US data on a one-month basis, a broader look at employment momentum in each country tells a different story.

US employment growth was robust throughout 2024. The US labour market can be classified as tight, and it is a potential source of near-term US inflation pressure.

Canadian employment growth wasn’t nearly as strong last year. Our labour force expanded rapidly due to high levels of immigration while our economic momentum slowed. That meant that our supply of labour easily outpaced our economy’s demand for it. (Our unemployment increased by 1% in 2024.)

That labour surplus gives the Canadian economy more room for non-inflationary growth and means that last month’s strong data shouldn’t impact the BoC’s rate-cut plans to nearly the same extent as the Fed’s.

Canadian bond-market investors seemed to agree. Although they did pare their bets on a BoC rate cut at its January 29 meeting a little, they are still giving slightly better than 50% odds that it will materialize.

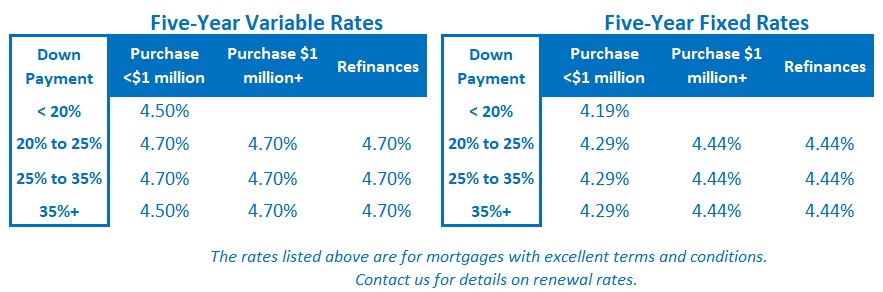

Note: If you are in the market for a mortgage today and want my take on the best options currently available, check out the section labelled Mortgage Selection Advice For Early 2025 in my blog post from last Monday.  The Bottom Line: Government of Canada bond yields surged higher last Friday, and that has put upward pressure on our fixed mortgage rates.

The Bottom Line: Government of Canada bond yields surged higher last Friday, and that has put upward pressure on our fixed mortgage rates.

If bond yields rise much more, expect a round of fixed mortgage rate increases to follow. (The release of the latest US CPI data, due out this Wednesday will likely provide the next catalyst.)

I continue to believe that the BoC will cut by another 0.25% on January 29. If that happens, our variable mortgage rates will decrease by the same amount shortly thereafter. The Bank’s policy rate currently stands at 3.25%, and that is still too high for our current economic backdrop.