How the Latest US Economic Data Have Impacted Fed Rate Cut Prospects

August 19, 2024Why the Bank of Canada Should Cut by 0.50% This Week

September 3, 2024

Last week saw encouraging developments on both sides of the 49th parallel for anyone hoping that Canadian mortgage rates will continue to drop.

We learned that Canadian inflation continued to cool in July, and US Fed Chair Jerome Powell used a speech in Jackson Hole, Wyoming, which hosts an annual three-day economics conference for central bankers, to emphatically pivot the Fed into rate-cut mode.

Here are the highlights surrounding both key developments along with my take on the implications for both our fixed and variable mortgage rates.

The Latest Canadian Inflation Data (for July)

On Tuesday Statistics Canada confirmed that our Consumer Price Index (CPI) rose by 2.5% on a year-over-year (YoY) basis in July, down from 2.7% in June and bang on the consensus forecast.

Our CPI is now the lowest it has been since the start of the pandemic, and, encouragingly, Stats Can also assessed that last month’s deceleration was “broad-based”.

The Bank of Canada’s (BoC) most closely watched measures of core inflation also came in lower last month. (CPI-trim fell from 2.8% in June to 2.7% in July YoY, and CPI-median decreased from 2.6% to 2.4%.)

Most of our remaining inflation pressure is still coming from shelter costs, which increased by 5.7% YoY in July overall. Within that component, rents increased by 8.5% YoY last month, and mortgage interest costs were up 21% over the same period.

Economist Ben Rabidoux of Edge Analytics noted last week that mortgage interest costs accounted for 1.2% of last month’s total CPI increase of 2.5%. It won’t be lost on the BoC that further rate cuts will directly reduce the inflation pressure coming from mortgage interest costs.

The BoC estimates that the neutral range for its policy rate, which is the level where it neither restricts growth nor stimulates it, is between 2.5% and 3%. The Bank has only reduced its policy rate from 5.0% to 4.5% thus far, so there is plenty of room for more cuts on the near horizon.

Another month of cooling inflation gives the BoC plenty of leeway to continue cutting. Deteriorating economic data, around everything from spending and employment to business investment and confidence indicators, increase the urgency for the Bank to take its foot all the way off the brake.

Simply put, the Canadian economy no longer needs (or is benefitting from) the tight monetary policy conditions that remain in place.

Fed Chair Powell Puts His Cards on the Table at Jackson Hole

Last Friday in a key speech at Jackson Hole, US Fed Chair Jerome Powell left no doubt about the Fed’s near-term plans.

Instead of the usual ifs, ands, and buts, that we have grown accustomed to when discussing the potential for rate cuts, Powell’s guidance was refreshingly blunt: “The time has come for policy to adjust. The direction of travel is clear, and the timing and pace of rate cuts will depend on incoming data, the evolving outlook, and the balance of risks.”

While he didn’t come right out and say that the Fed would cut at its next meeting on September 18, bond market investors are now assigning a 100% probability of that occurring. The only matter still being debated is whether the Fed will cut by 0.25% or 0.50%.

US bond market investors are currently assigning about a 75% chance that the Fed will cut by 0.25%. If the Fed cuts by 0.50% instead, US Treasury yields will likely fall. They will almost certainly take Government of Canada (GoC) bond yields (which our fixed mortgage rates are priced on) along for the ride.

US financial expert John Mauldin recently noted that the Fed has started five of its last six rate-cut cycles with a 0.50% cut. He believes that “a weak or even merely soft unemployment number for August” will be enough to push them in that direction, especially after we just learned that the US Bureau of Labor Statistics over-counted US job creation by 818,000 over the past twelve months (!).

Canadian variable-rate borrowers wouldn’t see the same immediate benefit from a 0.50% surprise cut by the Fed. But it would certainly give the BoC increased leeway to enact a 0.50% cut of its own by reducing the gap between the Fed and BoC policy rates.

Mortgage Selection Advice for Now

My overall assessment of our current mortgage-rate backdrop is unchanged from last week.

As economic downside risks on both sides of the 49th parallel increase, so too do the odds that today’s variable rates will outperform today’s fixed-rate mortgage options.

While variable-rate borrowers must accept a higher initial rate, their rates will fall in lockstep with each BoC rate cut. Fixed-rate borrowers will have to wait until the end of their terms for any rate reduction. In a falling rate environment, the faster your rate resets, the sooner you benefit. I still don’t think the BoC will stop cutting rates until it reduces its policy rate to at least 3%. (US bond market investors are currently positioned for the Fed’s policy rate to also be down to 3% by the end of 2025.)

All that said, while the case for variable rates is compelling, there are myriad factors that determine the direction of mortgage rates, and things don’t always work out as expected.

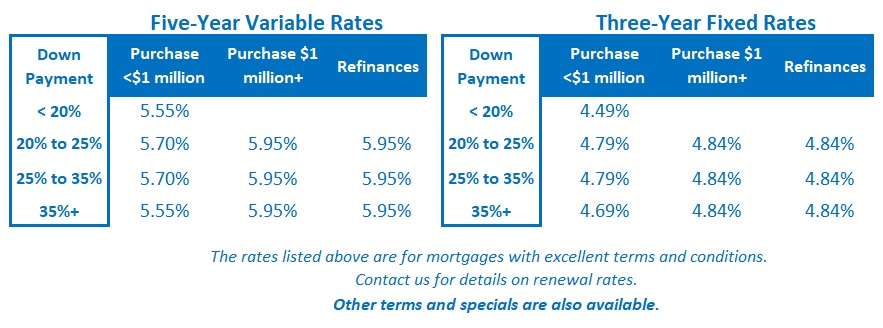

If you prefer the stability of a fixed interest rate, I think you are well advised to consider shorter fixed-rate terms today. While five-year fixed rates are the lowest on offer, I worry that five years is too long to lock in when rates are still near their recent peak.

If you are leaning towards a fixed rate, you should also pay extra attention to the terms and conditions in your mortgage contract. They vary widely among lenders and can have a surprising impact on the overall cost of your loan, especially if rates drop significantly during your term.

If you want to learn more about this topic, my post entitled What’s in the Fine Print is a good place to start. It provides a detailed summary of the terms and conditions to watch out for and links to other posts that dive deeper into the most important ones. The Bottom Line: Government of Canada bond yields continued to trend lower last week. Not enough to lead to another round of cuts to our fixed-rate mortgages but enough to bolster my belief that their next move will be down.

The Bottom Line: Government of Canada bond yields continued to trend lower last week. Not enough to lead to another round of cuts to our fixed-rate mortgages but enough to bolster my belief that their next move will be down.

Variable mortgage rate discounts have tightened of late. Despite that, all signs point to another BoC rate cut at its next meeting on September 4 and to several more cuts thereafter.